What is FIRE:

If you are not fimilar with FIRE it’s an acronym for Financial Independence Retire Early. It all started with a document called the Trinity Study (original copy if you are interested). The basic idea is that you save a bunch of money by living frugally, and invest that money into the a combination of stocks (mostly index funds not individual stocks) and bonds. Then you can safely withdraw 4% each year and live off that.

The 6 types of FIRE:

Surprisingly, I couldn’t find a complete list of the different FIRE strategies anywhere else, so I wanted to make my own. Note: We’ll be using a 4% safe withdraw rate (SWR) for the following calculations.

Barista FIRE – You are only going to semi-retire to reach financial independence faster and will rely on your portfolio growing over time through market growth.

Coast FIRE – You are going to let your net worth grow with your investments and cover your expenses with your income.

Lean FIRE – You are going to spend less than 40K USD per year / have saved 1M or less.

FIRE – You are going to spend between 40K and 100K USD per year / have saved between 1M and 2.5M.

Chubby FIRE – You are going to spend between 60K and 160K USD per year / have saved between 1.5MM-4MM.

Fat FIRE – You are going to spend more than 100K USD per year / have more then 2.5M saved.

My favorite FIRE calculator: https://www.playingwithfire.co/retirementcalculator

My personal FIRE plan:

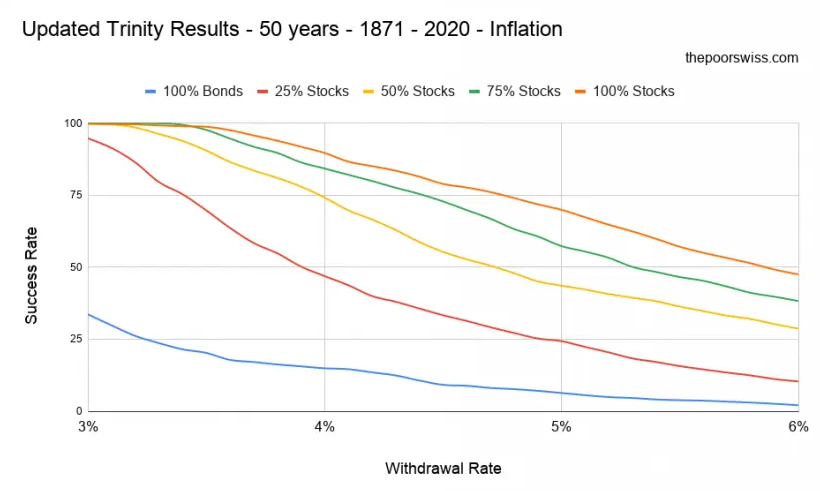

Recently the Trinity Study was revisited by ThePoorSwiss. The entire article is great and I recommend you read it, but for myself this is the most interesting chart:

Since I’m personally planning on retiring in my mid 30’s. I want to make sure that FIRE will work for me long term. I’m probably going to start at 95% stocks and 5% cash and over the years slowly transition into 80% stocks, 15% bonds, and 5% cash.

I’m still unsure of exactly what to invest in – Will VOO / VGT work for stocks? VTSAX for stocks and VBTLX for bonds is very interesting to me and will require more research.

Who knows what the market will do over 50+ years. What concerns me is that 4% may not work for me, so I’m setting my SWR at 3.5% for the most chance of success.

Recommend reading:

Updated Trinity Study for 2021 – More Withdrawal Rates!